Development of multi-component cost management system for organizing and conducting Research and Development

Разработка многокомпонентной системы управления затратами на организацию и проведение научно-исследовательских и опытно-конструкторских работ

Desarrollo de un sistema de gestión de costos de componentes múltiples para organizar y realizar trabajos de investigación y desarrollo

Abstract

The article is devoted to the process of developing a multi-component cost management system for organizing and conducting Research and Development (R&D). The analysis of the current level of funding for science from funds allocated by the federal budget and funds provided by private organizations. The article discusses the concept of R&D as an integral object of management, clarifies the content of the concept of "cost management system for R&D". It is concluded that the modern cost management system for organizing and conducting R&D should be considered as a multi-level target information system. The goal of R&D cost management system has been determined, which is to optimize the size and structure of R&D costs in order to qualitatively improve the performance indicators of a high-tech enterprise by organizing R&D cost management. The author proposes a multicomponent cost management system for organizing and conducting R&D, based on the integration of various approaches, concepts and methods of organizing cost management in the implementation of basic management functions. The results of the research carried out in the article can be used as a theoretical basis for building a multicomponent cost management system in modern high-tech enterprises.

Keywords: enterprise cost management, research and development, organization of planning in the field of research and development, cost accounting, intellectual property, regulatory costs, effective management of high-tech projects.

Аннотация

Статья посвящена процессу разработки многокомпонентной системы управления затратами на организацию и проведение НИОКР. Проведен анализ текущего уровня финансирования науки из средств выделяемых федеральным бюджетом и средств предоставляемых частными организациями. В статье рассмотрено понятие НИОКР как целостного объекта управления, уточнено содержание понятия «система управления затратами на проведение НИОКР». Сделан вывод, о том что современную систему управления затратами на организацию и проведение НИОКР следует рассматривать как многоуровневую целевую информационную систему. Определена цель системы управления затратами на НИОКР, которая заключается в проведении оптимизации размера и структуры затрат, приходящихся на НИОКР с целью качественного повышения показателей эффективности работы высокотехнологичного предприятия за счет организации управления затратами на НИОКР. Автором предложена многокомпонентная система управления затратами на организацию и проведение НИОКР, основанная на интеграции различных подходов, концепций и методов организации управления затратами при реализации основных управленческих функций. Результаты проведенного в статье исследования могут использоваться в качестве теоретической базы для построения многокомпонентной системы управления затратами на современных высокотехнологичных предприятиях.

Ключевые слова: управление затратами предприятия, проведение научно-исследовательских и опытно-конструкторских работ, организация планирования в сфере НИОКР, учет затрат, объект интеллектуальной собственности, нормативные затраты, эффективное управление высокотехнологичными проектами.

Resumen

El artículo está dedicado al proceso de desarrollo de un sistema de gestión de costos de componentes múltiples para organizar y realizar Investigación y Desarrollo (I + D). El análisis del nivel actual de financiación para la ciencia a partir de fondos asignados por el presupuesto federal y fondos proporcionados por organizaciones privadas. El artículo analiza el concepto de I + D como objeto integral de gestión, aclara el contenido del concepto de "sistema de gestión de costes para I + D". Se concluye que el moderno sistema de gestión de costos para organizar y realizar I + D debe considerarse como un sistema de información de objetivos de varios niveles. Se ha determinado el objetivo del sistema de gestión de costes de I + D, que es optimizar el tamaño y la estructura de los costes de I + D para mejorar cualitativamente los indicadores de rendimiento de una empresa de alta tecnología mediante la organización de la gestión de costes de I + D. El autor propone un sistema de gestión de costes multicomponente para organizar y realizar I + D, basado en la integración de varios enfoques, conceptos y métodos de organización de la gestión de costes en la implementación de funciones básicas de gestión. Los resultados de la investigación realizada en el artículo se pueden utilizar como base teórica para construir un sistema de gestión de costos multicomponente en empresas modernas de alta tecnología. Palabras clave: gestión de costes empresariales, investigación y desarrollo, organización de la planificación en el campo de la investigación y el desarrollo, contabilidad de costes, propiedad intelectual, costes regulatorios, gestión eficaz de proyectos de alta tecnología.

Palabras clave: gestión de costes empresariales, investigación y desarrollo, organización de la planificación en el campo de la investigación y el desarrollo, contabilidad de costes, propiedad intelectual, costes regulatorios, gestión eficaz de proyectos de alta tecnología.

Introduction

Scientific and technological progress is a constant and continuous process taking place in two parallel areas: updating scientific knowledge and changing production technology, taking into account the nature of the operation of technological equipment. Scientific and technological progress has a significant impact on the entire production sector, qualitatively contributes to an active increase in labor productivity and the efficiency of the production process, accelerating the pace of social and economic development of the country. The result of the influence of scientific and technological progress on production and technological areas is innovation. At the turn of XX and XXI centuries, the role of innovations changed, which began to act as the main factor in the socio-economic development of countries, as well as a relation between innovations and the economic sphere. The modern stage of economic development is characterized by the influence of science on various reproduction processes. Developed countries and high-tech enterprises are systematically increasing funding for various R&D.

Innovative enterprises play a decisive role in the development of the Russian economy and make a significant contribution to the formation of GDP. For this, an innovative enterprise must have significant potential and maintain high rates of R&D at the level of world indicators, which is realized through: performing competitive R&D, effective management of results and accelerating their involvement in economic turnover. The creation of an effective organizational and economic mechanism for managing R&D is a necessary component of the success of an innovative high-tech enterprise (Bogacheva & Feoktistova, 2016). Eliminating the fragmentation of the management of the scientific space and increasing the level of integration of science and production, by involving the results of R&D in the economic turnover of an innovative enterprise are the most important conditions for the competitive development and financial and economic survival of an innovative industrial enterprise in the conditions of market relations. For effective management of R&D, it is necessary to offer complex procedures and solutions from the ordering stage to the use of the results. At the same time, the developed organizational and economic mechanism for R&D management should ensure a transition to more meaningful and high-level decision-making processes, accelerate and unify R&D management processes.

Literature Review

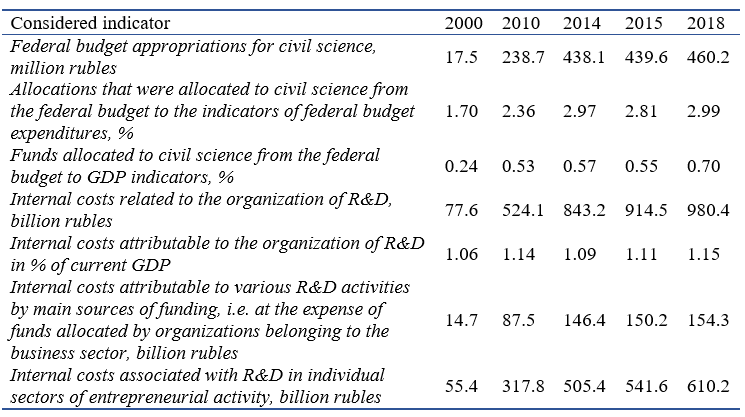

Russia lags behind the leading countries of the world in terms of the degree of funding for R&D, and the implementation of the national project "Science" practically does not change this situation, since the expenditures on science indicated in the framework of this national project are insufficient for the innovative development of the economy. Experts from the Accounts Chamber analyzed the main reasons that, in their opinion, are holding back scientific development in Russia. To date, Russia is confidently ranked among the world scientific leaders in only one parameter: the absolute scale of employment in science. The number of Russian researchers in 2018 amounted to 514.7 thousand people, moreover, only in China (about 1.9 million people), USA (about 1.7 million people) and Japan (794 thousand people). Even if the target parameters are achieved within the framework of the national project "Science", spending on science in Russia will grow by 2024 to only 1.2% of GDP. In China, spending on science is about 2.2% of GDP, in the United States - 2.9% of GDP and in Germany - 3.0% of GDP (Kolesnik et al., 2015). We consider in more detail the main indicators showing the level of financing of modern Russian science (Table 1).

Table 1.

Structural composition of the main indicators of the level of financing of Russian science.

In the current conditions of the gradual transition of the Russian economy to a fundamentally new innovative path of development, there is a certain trend associated with an increase in demand for various high-tech products, which means that the development of competitive high-tech industrial products should become a priority task for high-tech enterprises. The amount of R&D costs is one of the main indicators that determines the degree of efficiency of scientific and technical activities carried out by the enterprise. The low economic efficiency of public and private investments in the development of science-intensive products is caused by a weak methodological base, the lack of effective tools and methods for managing the costs of organizing and conducting R&D at enterprises. It should be noted that R&D costs are the most difficult to manage and forecast. We consider the main factors that affect the value of innovation costs (Eremeeva, 2017):

- scale of the tasks to be solved;

- amount of costs increases proportionally depending on the current stage of innovation process;

- emerging need for the costs of related industries associated with the direct implementation of various innovative solutions;

- existing need to organize the transition to a fundamentally new technical principle of effective problem solving;

- size of the designed object;

- current level of tariffs, prices and rates for various types of resources that are used in innovation processes related to the implementation of organizational and legal actions;

- level of radicality of the proposed innovations;

- influence of the time factor on the accuracy of the planning process, depending on the timing of the project;

- level of development of tools and effectiveness of management of various types of costs.

Materials and Research Methods

The methodological and theoretical basis of the research is based on the works of Russian and foreign scientists. In the course of the research, the following methods were used: content analysis of regulatory and legal documents, analysis of fundamental and theoretical provisions presented in modern literary sources and systematic approach in the study of research problems (Kovyrzina & Guseva, 2019). The purpose of the research carried out in the article is to develop a multicomponent system for organizing and managing R&D costs of a high-tech enterprise, focused on high-quality and efficient use of a limited amount of resources, a qualitative increase in the level of competitiveness and competent solution of various strategic tasks.

The current problem in the field of cost management is very relevant and significant, therefore, Russian and foreign scientists conduct various scientific research in this subject area. Despite the huge range of scientific research in the field of cost management in scientific works, very little attention is paid to issues related to the formation of a cost management system in the field of R&D in modern high-tech enterprises (Komonov et al., 2018). In the course of the study, an analysis of special and scientific literature was carried out, including the study of special management practices for managing costs for Russian high-tech enterprises, which led to the conclusion that there was an insufficient degree of methodological and theoretical developments regarding the development of a multi-component R&D cost management system. The existing approach to organizing and managing costs at high-tech enterprises is characterized by unsystematic and fragmented nature, and those responsible for making managerial decisions do not have complete and accurate information about the level of R&D costs, which also affects the choice of the most effective managerial decision. The linear-functional structure applicable to most enterprises tends to best implement management functions such as accounting and planning, but other cost management functions are performed only partially or not represented at all (Peresypkina et al., 2017).

The cost management system for organizing and conducting R&D is a subsystem of the management system of a high-tech enterprise, in which the object of management is the costs that arise in the process of direct implementation of R&D, and the subject of management in this case is the heads of various levels. This system is focused on the implementation of a whole range of targeted actions in the field of optimizing the costs of R&D, the formation of an information on current R&D costs for management entities, for a qualitative increase in the efficiency of the current activities of a high-tech enterprise, which is fully carried out scientific and technical activities. The proposed R&D cost management system should be considered as a single multicomponent information system, which is not only a management subsystem, but also interactions between various components. A cost management system for R&D is necessary to effectively optimize the structure and size of costs for organizing and conducting scientific research. We consider the structure of the mechanism for managing the costs of organizing and conducting R&D (Tretyakova et al., 2019):

- changes in the financial structure of a high-tech enterprise with the subsequent allocation of places where certain costs and centers of financial responsibility appear;

- design of information flows in order to ensure the continuous collection and transmission of information, which contains information about the current costs of R&D;

- R&D project should take into account the necessary costs for its implementation;

- accounting of costs by centers of financial responsibility and cost items;

- implementation of cost control in order to detect possible deviations of actual values from planned values;

- time analysis of cost structure changes, including benchmark analysis;

- making management decisions by the enterprise management.

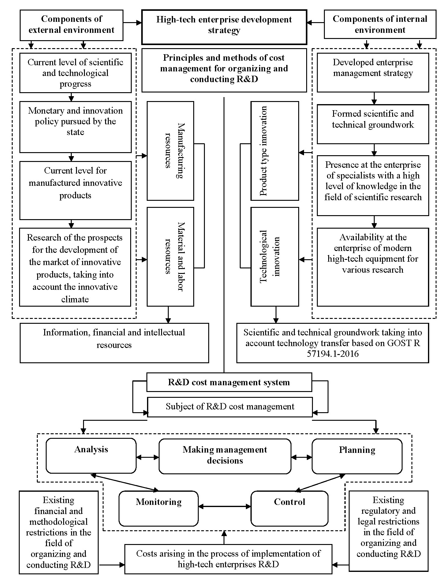

A key distinctive feature of the system being developed for managing costs for organizing and conducting R&D is the presence in it of two objects of management: costs associated with product development and costs of product design at R&D stage. The model of R&D cost management system proposed in the article is based on the use of the "white box" model and is shown in the Figure 1. The proposed model of R&D cost management system describes the operation of three subsystems: control subsystem, which is the subject of management, controlled subsystem, which is the object management and subsystem of functions and connections. A multi-component R&D cost management system includes:

- Conducting marketing research of the target costing market:

- target cost of the designed product has been determined:

- set the target cost of R&D.

- Carrying out a technical and economic examination of the developed project based on the parametric method:

- forecasted cost of the designed product was determined.

- Estimation of the cost of alternative options for the implementation of the project in the field of R&D based on the application of the calculation-expert method:

- determination of planned costs for alternative options for carrying out work in the field of R&D.

- Assessment of the most effective options for conducting R&D based on the method of the most preferred option for performing R&D:

- most preferred R&D option has been identified.

- Determination of limits for each stage and calculation items of the developed project in terms of R&D:

- approved limits for each specific stage and costing items.

- Carrying out accounting for technological and scientific preparation of production based on the method of accounting for costs and limits for each separate stage and calculation items:

- actual costs required for R&D are determined.

- Control over the costs associated with the implementation of technological and scientific preparation of production, based on the use of the method of current cost control:

- receiving data on changes and deviations in the established limits.

- Analysis of current costs for technological and scientific preparation of production, based on the use of factor analysis and index method:

- identification of the culprits of deviations and making certain decisions on them.

- Making a decision to start serial production of a standard-costing product developed at the enterprise:

- standard cost of the product for mass production has been determined.

Figure 1. Model of cost management system for organizing and conducting R&D.

The proposed approach to creating a multicomponent cost management system for organizing and conducting R&D is based on the consistent integration of various approaches, concepts and methods of cost management, provided that the main management functions are consistently performed, namely, accounting, control, analysis and management decision-making (Pavlova & Muratova, 2018). The concept of "target-costing" is an effective method in the field of cost management, which allows the management of the enterprise to successfully implement the functions related to planning and preventive control of the costs of the designed product and also allows the calculation of the target cost. Implementation of the “target-costing” concept in this system provides for its orientation towards two important indicators: target price of designed product and target cost of R&D project. Based on the obtained data on the target price of the designed product, the most preferable level of profit obtained from the sale of a new product is determined, and then the target cost of the product is determined, while the indicator of the target cost of the product is the maximum possible cost of the product. Carrying out a technical and economic examination of the project allows establishing the predicted cost of the designed product based on the use of the parametric method. If the indicator of the projected cost is higher than the indicator of the target cost, then it is necessary to determine the categories of costs to be optimized or reduced through the use of functional cost analysis. As a result of the application of the functional cost analysis, the target cost level should be achieved, but if this did not happen, then we need to go to the cost estimation stage and re-analyze the alternative project options in terms of R&D. Otherwise, the possibility of a complete refusal to carry out an R&D project is allowed (Novikov & Sazonov, 2020).

Results

Based on the data obtained on the projected sales volumes of the product developed at the enterprise and the requirements of the accounting policy, the target cost of R&D project is established. The indicator of the target cost of a project in the field of R&D is the maximum possible size for investment in R&D project under development, at which the profitability of the designed product is maintained. On the basis of the requirements for the designed product, which were set out in the terms of reference, options for the possible implementation of a project in the field of R&D are determined, taking into account the required amount of costs for their implementation. Then it is necessary to determine the most effective option for the implementation of R&D project, taking into account that its implementation is associated with indicators of economic efficiency, therefore, the indicator of the planned cost of alternative options for implementing R&D was less than / equal to the target cost of R&D, which was determined at the first stage. After choosing the optimal variant of the project in the field of R&D for its implementation on the basis of the schedule approved by the enterprise management, the process of allocating resources begins, taking into account the designated limits for each separate stage and calculation items. Organization of cost control in terms of R&D is proposed to be carried out on the basis of the use of the method of current control for the main changes and deviations. Before a decision is made to start a serial launch of a product developed at the enterprise, based on actual production data on the costs of R&D, the costs associated with the preparation of production and the development of the necessary technologies, it is necessary to clarify the indicators of the planned cost of production based on the "standard-costing" method. If the indicator of the planned cost of the product turns out to be less than or equal to the target indicator, then we need to make a decision on the start of serial production, otherwise we need to determine whether it is possible to achieve the target cost at the stage of serial production of the product, this can be done if we apply the concept “kaizen-costing". If the target cost cannot be reached at the stage of mass production, it is advisable to completely abandon the production of this type of product.

Conclusions

In modern conditions, when the Russian economy is switching to an innovative path of development, the process of enhancing the innovative activities of high-tech enterprises is the main condition for ensuring their survival in the face of intense competition. The main task that is set for Russian high-tech enterprises, which are actively engaged in the implementation of various R&D, is the creation and subsequent introduction into production of new unique types of science-intensive products. In these conditions, a special role is played by the organization of effective cost management for the organization and conduct of R&D within the enterprise. In conditions of insufficient funding for various R&D, enterprises need to carry out applied R&D only at their own expense. The proposed approach to the design of a multicomponent cost management system for organizing and conducting R&D is distinguished by the presence of an interconnected implementation of all basic management functions, as well as ensuring a stable relation between R&D cost management and the organization of cost management at all other stages of the product life cycle, this is achieved due to the presence of two objects cost management. The set of approaches, concepts and methods proposed in the article in the field of organizing R&D cost management will give a certain opportunity for the effective management of the scientific and technical activities of a high-tech enterprise, which will allow making high-quality management decisions at each separate stage of the implementation of proactive R&D.